So Fresh, So Clean

“Ain’t nobody dope as me, I’m just so fresh, so clean”

–So Fresh, So Clean, OutKast, 2000

Gator belts and patty melts. The U.S. stock market remains on one helluva ride in 2025. After starting the year on a December through February consolidation grind, worries about tariffs that eventually were manifested sent the S&P 500 on a -21% tumble through early April. But after giving new fiscal policy meaning to the old monetary policy trope “the pause that refreshes”, the headline index has been vaulting to the upside ever since. While trading less than +4% above it’s previous mid-February highs, the U.S. stock market is back to vibing with swagger. This is fresh and clean and all, but is it real? And is it sustainable?

Feeling like Rollo. The U.S. stock market continues to come alive as we continue through the second half of the year for good reason. One has to look no further than the latest on corporate earnings to see why the market is exuding style and confidence. The earnings outlook has always been strong in 2025 running in the low double-digits, but remember when earnings season was getting underway a little over a month ago and the financial news media started wringing their hands about the potential for slowing profit growth coming out of 2025 Q2 earnings season? Yeah, not so much.

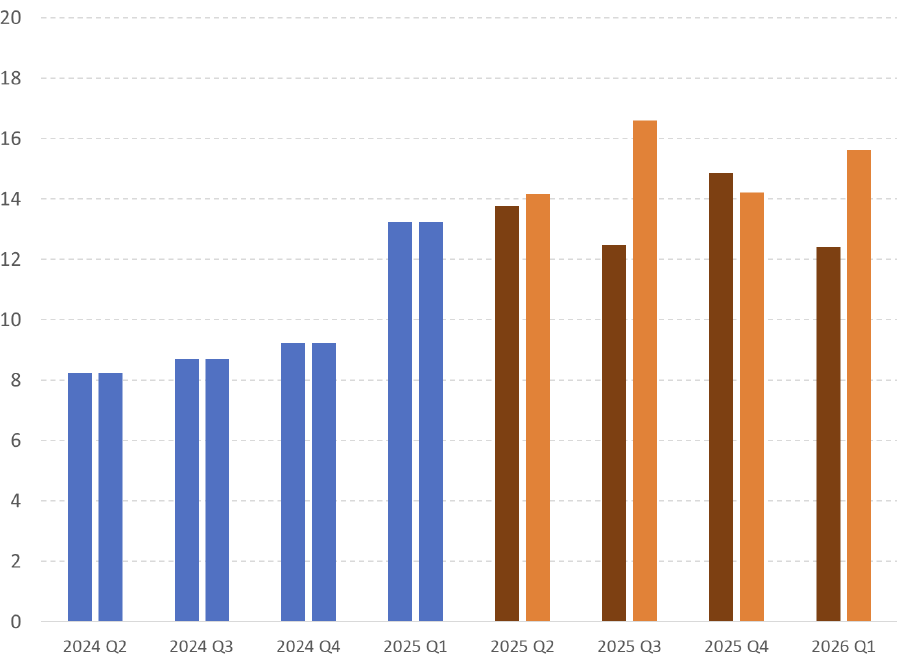

Check it. At the start of 2025 Q2 earnings season, the actual profit growth forecast for the next four quarters is shown in the chart below by the dark red bars. Rock solid in the 12-15% (I’m still puzzling on where everyone was getting the 5%ish growth estimates heading into earnings season. C’mon!). Where are we today coming out of earnings season with roughly 80% of companies having reported? While companies typically revise their profit outlooks lower the closer the future draws closer to reality, they instead revised their already lofty outlooks higher as shown by the orange bars below to the 14-17% range. Showtime at the Apollo indeed!

S&P 500 Annual As Reported Earnings Growth (%)

12 Month Earnings Per Share As Of 8/6/2025

Historical data in blue, forecasted data in red and orange

Source: S&P Global

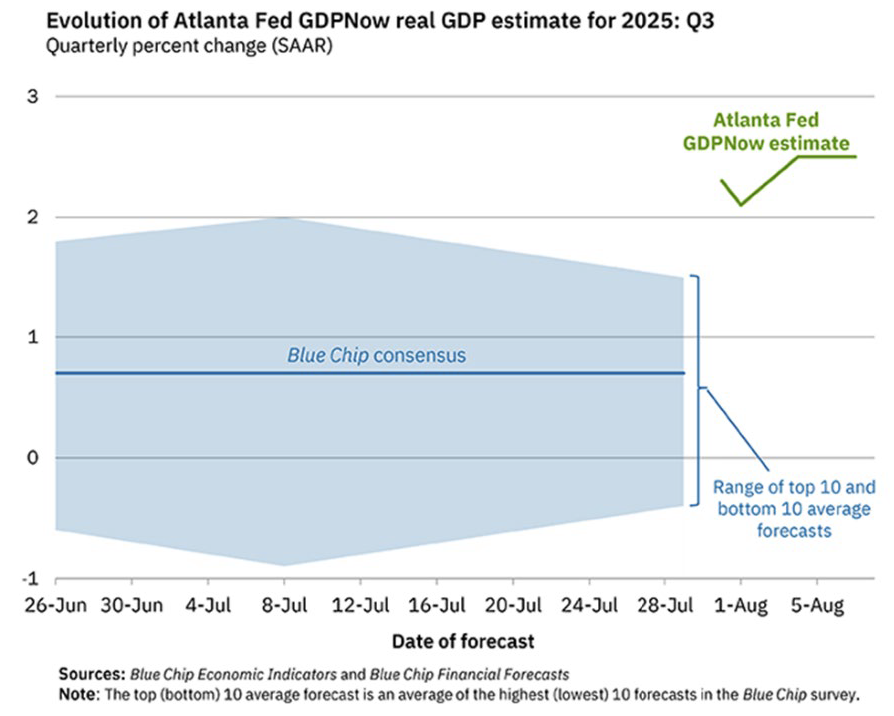

Let’s dig a little deeper into the fundamentals. Keeping it clean, here is an early look at the Atlanta Fed GDPNow forecast for 2025 Q3. So fresh at +2% coming out of the gates for the current quarter based on the data, once again well ahead of more pessimistic “blue chip” economist expectations at a time when green, green from the Atlanta Fed in the chart below has been getting it right and blue from the economists has been getting it wrong.

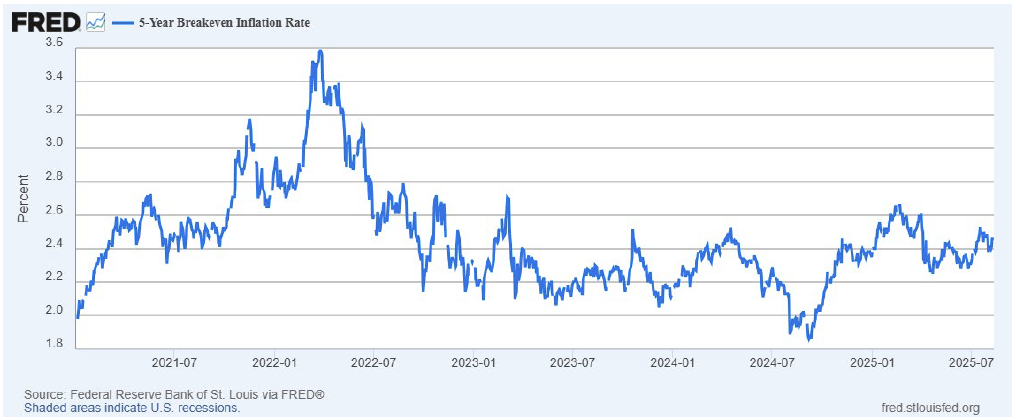

What about inflation expectations? Inflation, after all, continues to be the primary downside risk for financial markets as we move through the second half of 2025. The answer, pricing pressures remain cooler than sippin’ a milkshake in a snowstorm.

Putting all of this together, all of the core elements to drive stock prices higher – solid economic growth, steadily low inflation, and corporate profit growth – are firmly in place. Ain’t nobody as dope as the U.S. stock market right now.

(In my mind) the sky is falling. With all of this stock market style and swagger, what could possibly go wrong? Remember, this is the U.S. stock market that we’re talking about. Yes, it has a track record of rising relentlessly over time (never mind the nominal period from 2000 to 2012, the inflation adjusted period from 1966 to 1982, or the inflation adjusted price performance from 1929 to 1986 for that matter – so stale, so dirty? Insert thinking emoji here), but it is not without the types of risk that can send it spontaneously into a bear market and back in lightning speed like it did, oh yeah, just a few months ago.

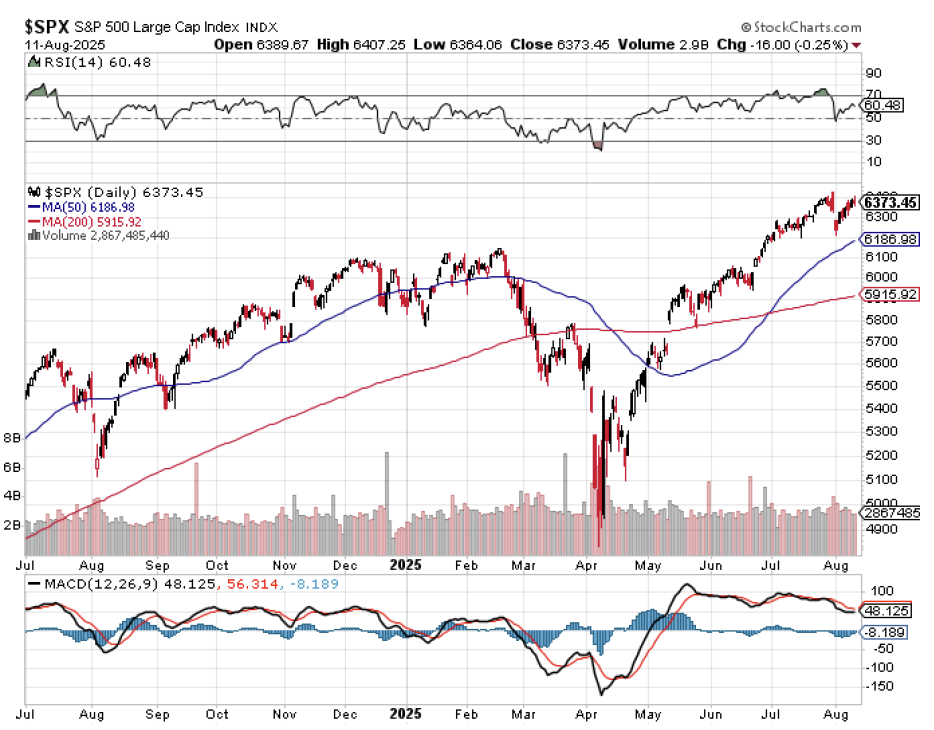

One thing that bugs me is the once again overdue need for some mean regression (mean being “average” that is, not “impressive” or “cool”, and also not “tough” or “intimidating” (or then again maybe on the latter)). Consider the chart below. Following the phenomenal rally since early April, the S&P 500 is once again trading ahead of itself trading 3% above its medium-term 50-day moving average (blue line), which is nearly +5% above its long-term 200-day moving average (red line), which is more than +5% above its ultra long-term 400-day moving average (pink line). Knowing that these trendlines like to converge over long-term periods of time, this means that we could see anywhere between a -9% to -14% pullback on the S&P 500 over a four to twelve week period at any time and it would mean nothing more than a mean reversion within a long-term uptrend that would remain firmly intact. I then think about calendar effects – we are, after all, in mid-August and now entering what is seasonally the worst performing time of year for the U.S. stock market through mid-October. While some years it’s awesome, other years like 2023, not so much.

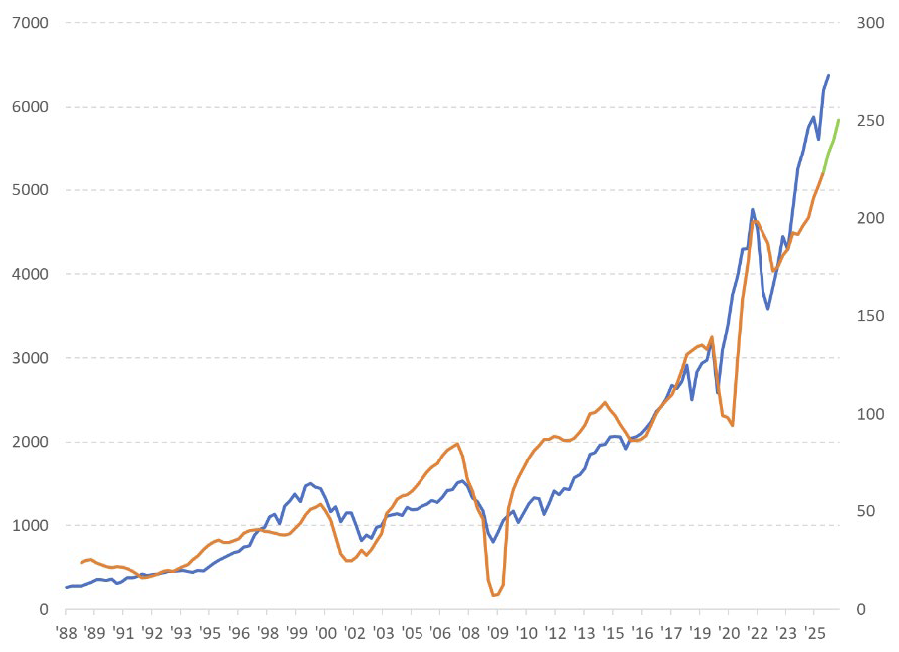

Also consider where we are relative to corporate earnings with the stock market today. Yes, earnings are rising, but the stock market as measured by the S&P 500 (blue line in chart below referencing the left axis) from a valuation perspective is running well ahead of its earnings implied price (12 month as reported earnings referencing the right axis in the chart below with the orange line being history and the green line the forecast – source for the data is once again S&P Global) at around 5200 today and 5900 at the end of the first quarter of 2026. It’s important to note that such a move would only take the S&P 500 down from an extraordinarily rich 28 times earnings to a still very rich 23 times earnings. Of course, valuations often do not matter for stocks until they do, which is around the time of an economic recession. With GDP growth projected to stay positive, this remains a worry for another day at least for now.

S&P 500 Index (L, blue line) vs. S&P 500 12-Month As Reported Earnings ($, R, orange line / green line forecast)

Source: S&P Global

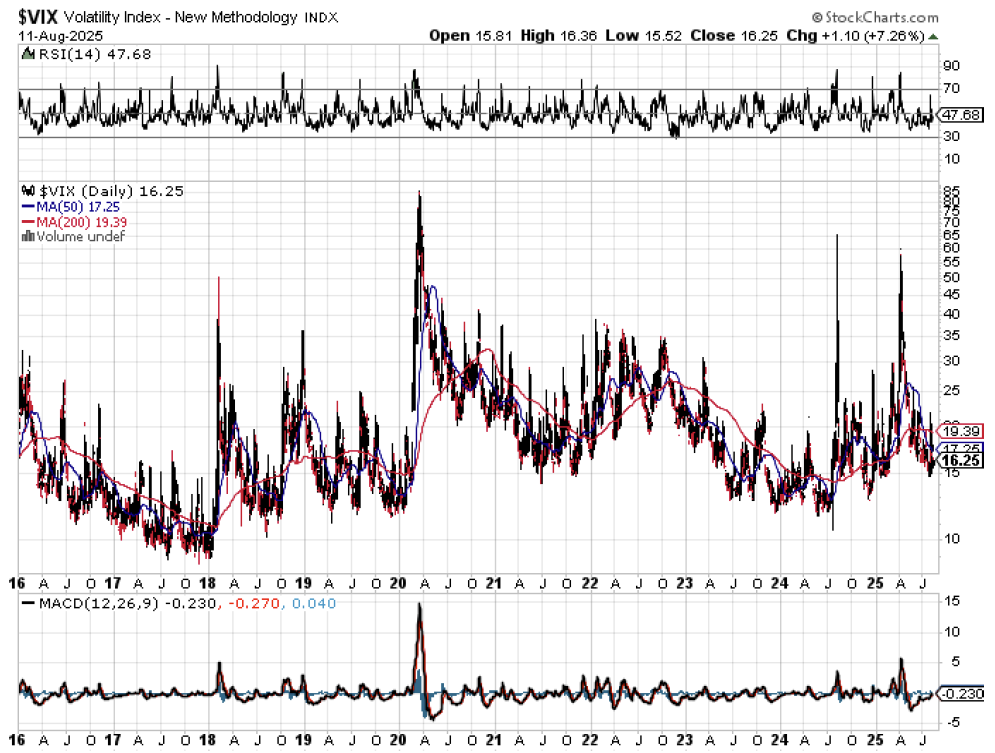

I then turn my attention to the CBOE Volatility Index, or VIX, which is a measure of “fear” in the stock market place. While we are not steadily operating at COVID period levels, the VIX remains elevated in the high teens and is not beyond spiking north of 60 over the past year, which is a stock market data way of saying that investors have had moments of super freaking out in recent months.

Get to running off at the mouth. This brings me to another worry. Don’t get me wrong, I get it. We live in an era of kayfabe politics in 2025 (unless we’re in the aftermath of a lost election – fleeting neokayfabe?). Washington DC has always been a performative stage, but now Reps, Senators, and Executives (and even some Judges) come packing chairs and the figure four leg lock to get their moment in the spotlight. It is important when watching the financial news and/or CNN, FoxNews, MSNBC to take everything we are hearing with a long reflective pause and a gigantic block of salt regardless of wherever you may reside on the political aisle (remember, the commentators on these networks are just as down with kayfabe as the pols they are reporting on – eyeballs must be attracted to sell advertising, after all). Nonetheless, the steady rumble of daily headline risk is set to continue for financial markets no matter how desensitized it may become.

More specifically, a paradox continues to unfold that also has the lingering potential to rattle financial markets in the weeks ahead. Here is the apparent contradiction. We’re supposedly living in the greatest economy ever since the formation of the solar system (wait a second, what about the 9-18 month response lag of fiscal policy on the U.S. economy? Does this mean that credit for today’s economic super strength is owed to the previous administration? Is this Chief Market Strategist going kayfabe himself!?! Nah. Frankly, whether the current leadership in Washington is Democratic, Republican, Green, Libertarian, or from Mars, their impact on growth is at best on the margins. Economy gonna economy – you largely get what you get when you’re in office). So why then are the calls out so aggressively for the U.S. Federal Reserve to cut interest rates? If everything is so awesome and we just passed a big, beautiful fiscal policy bill that’s going to make things even “awesomer”, shouldn’t the Fed be keeping their powder dry and not lower interest rates? In fact, shouldn’t the Fed be thinking about the possibility of raising interest rates to counterbalance the already strong backdrop we outlined above coupled with the additional fiscal stimulus coming down the pike. Clearly, there is no shortage of liquidity when meme stocks that are otherwise on a fast track toward bankruptcy start spiking by more than +200% in post COVID, GameStop-ish, 2021 style. Unnecessary rate cuts are how an economy and markets that are thriving today can quickly become derailed by a scorching case of inflation in a few months time. It is important to remember that the calendar flipped for the economy and financial markets from 2021 to 2022 not that long ago, and both monetary and fiscal policy makers from both sides of the political aisle had their fingerprints all over that inflation mess. Nonetheless, the Fed is set to cut interest rates by a quarter point according to today’s projections when they next meet on September 16-17. Stay tuned.

So fresh, so clean, but not without risk. The economy and financial markets are giving investors good reason for swagger and flex. Economic growth remains solidly positive, inflation pressures are under control, and corporate earnings are growing at a double-digit rate. But style and stride can lead to overconfidence. Not only is the market now once again overdue for a pullback, but downside risk catalysts remain that should be monitored closely as we continue through what is historically the most challenging months of the year for financial markets.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Investment advice offered through Great Valley Advisor Group (GVA), a Registered Investment Advisor. I am solely an investment advisor representative of Great Valley Advisor Group, and not affiliated with LPL Financial. Any opinions or views expressed by me are not those of LPL Financial. This is not intended to be used as tax or legal advice. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. Please consult a tax or legal professional for specific information and advice.

LPL Compliance Tracking #: 782357