10 Years Gone

Last week, I had the opportunity to visit our GVA Advisors in Boca Raton, Florida. This week’s article is inspired by the great conversation we had during our stay with some of our Advisor friends over dinner (one of which I look forward to potentially hearing play the guitar someday!).

“Then as it was, then again it will be

An’ though the course may change sometimes

Rivers always reach the sea”

–Led Zeppelin, Ten Years Gone, Physical Graffiti, 1975

The path of capital markets over the past decade is clear and definite. The U.S. stock market has dominated the stage, led by the biggest common stock stars of them all in the mega cap space. Growth has trounced value by nearly three times over this time period, with the greatest winners of them all coming specifically from the tech space. With so much good fortune coming from such a narrow segment of capital markets, it raises the question as to whether the principles of broad portfolio diversification have become trampled under foot. Despite the ten years gone, portfolio diversification is arguably as important as ever as we move through the next ten years from now.

“Blind stars of fortune, each have several rays

On the wings of maybe, down in birds of pray”

–Led Zeppelin, Ten Years Gone, Physical Graffiti, 1975

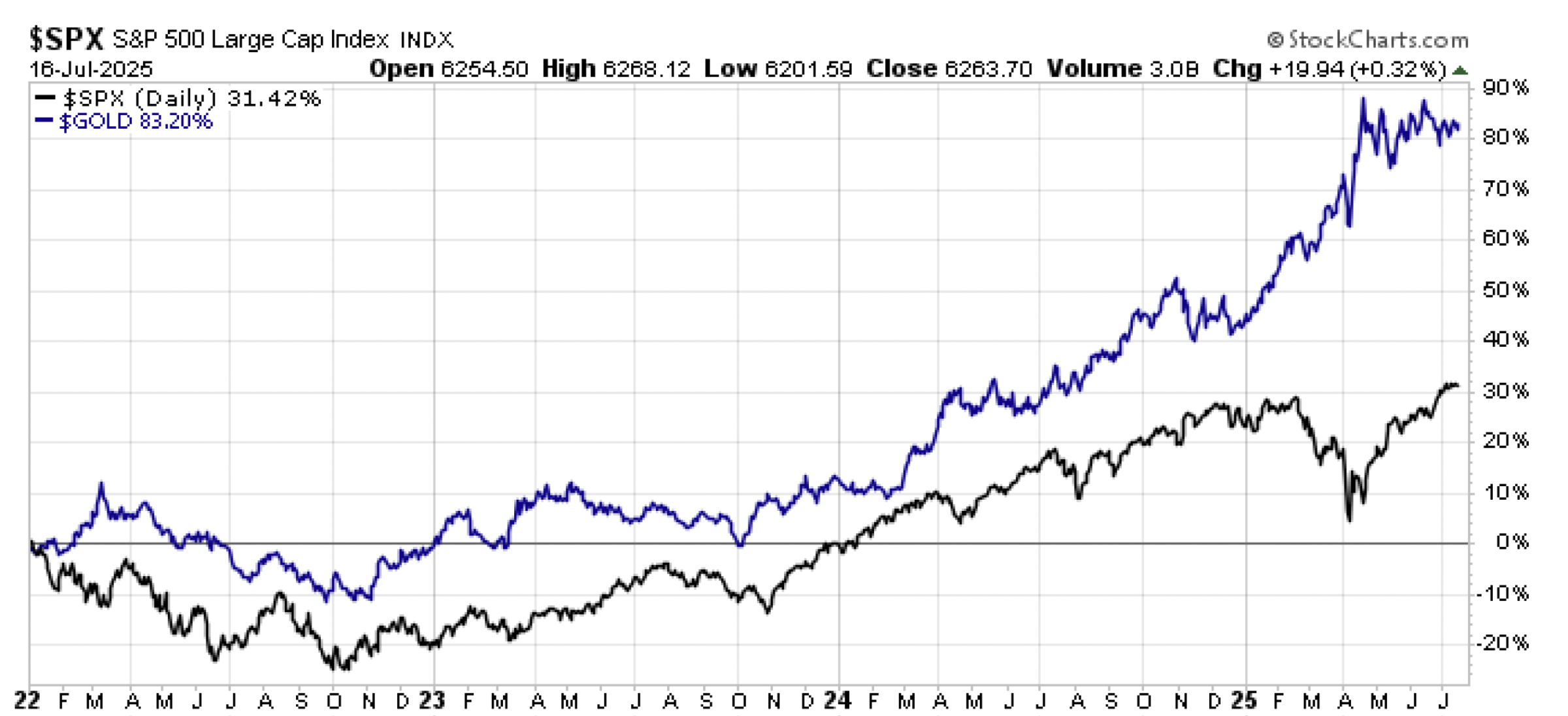

Indeed, a broad array of asset classes have relatively struggled over the past decade. This list includes the aforementioned value stocks along with U.S. mid-caps, U.S. small caps, developed international stocks, emerging market stocks, bonds, and precious metals. But just because they underperformed over the entirety of the last decade does not mean that they did not have their times of extended virtue along the way. For example, consider the performance of gold over the last three and a half years since the start of 2022 through today. Despite the phenomenal stock market run over this time period, the barbarous relic has generated nearly three times the return over this same extended period. And these results are coming from an asset that has comparable price volatility to the S&P 500 but travels a total return path along the way that is almost completely uncorrelated with a coefficient at +0.13. Much ballyhooed tech sector up +53% over this same time period, eat your heart out.

Nevertheless, I am reminded of the classic quote from an advisor who stood amid a restless audience at a national conference in September 2000 and boldly asserted the following rhetorical question to the presenter espousing broad portfolio diversification (no, it wasn’t me at the lectern that day, but my time was gonna come in the years that followed).

“We all know that technology stocks are going to dominate the market over the next ten years, so why then are we allocated to anything else in our investment portfolios?”

Umm. . .

I’m guessing down as much as -80% is not what bro had in mind. Ten years gone is a wicked understatement. But you know what performed really well and posted positive returns over this same 2000s time period? Value stocks, mid-caps, small caps, international stocks, precious metals, and commodities.

This highlights an important point. Winners across capital markets move in and out of favor over time. These phases are often secular in nature, which is why I’ll sometimes reference market cycles going back to the late 1800s because you need it to assess how conditions unfold and securities perform over multiple cycles that can last 17 years or more at a time on average in many cases. This doesn’t mean that mega cap growth tech stocks aren’t going to continue to kill it between now and 2035. But it also doesn’t mean that their not going to take a custard pie to the face either. Such are the continued wings of maybe confronting investors with every new capital market phase.

“Kind of makes me feel sometimes, didn’t have to grow

But as the eagle leaves the nest, it’s got so far to go”

–Led Zeppelin, Ten Years Gone, Physical Graffiti, 1975

Graffiti. You may have noted in the passage above the italicized emphasis on commodities. Talk about ten years gone for this woebegone asset class. Diversification? Indeed, with a low total returns correlation with the S&P 500 of +0.37. Di-“worse”-ification? Perhaps, with a cumulative return for commodities over this time period that is barely positive with marginally higher price volatility versus the S&P 500 that has been crushing it with double-digit annualized returns over the same time period.

Why even bother discussing such a moribund asset class after so many dismal years? Because it wasn’t always this way for commodities. And it may not be this way again over the next ten years.

Consider the period from 2000 to mid-2008. At a time when the cumulative return on the S&P 500 was negative, commodities were posting double-digit annualized returns fueled by robust global demand including most notably China. Remember watching CNBC in 2007 when everybody was buzzing about “rare earths” and were trying to get nailed down the correct pronunciation of molybdenum? It wasn’t because commodities were performing poorly at the time (hear anyone on the telly lately trying to wrestle out the name dysprosium? Yeah, me neither).

So why even consider commodities today? It’s not because the price of commodities like copper and cocoa have outperformed a U.S. stock market that has been raging in its own right since the start of 2024. That’s anecdotal. Instead, it’s because the four-decade bull market in bonds ended back in 2022 for a reason. It’s because higher inflation is likely here to stay for the foreseeable future. It’s because a world that once seemed destined for perpetual globalization kumbaya in the years immediately following the end of the Cold War (remember Bush sharing a now notorious barbeque with Putin back in the day? “I looked into his eyes and I saw a soul. I trusted him”. Insert ironically pensive emoji in 2025 here (not a politically partisan knock mind you, as I could riff on Obama-Putin material just as easily too – remember the 2012 Presidential debate? I guess that “call from the 1980s” was answered after all – ooof)) is increasing retrenching toward disglobalization if not outright deglobalization and regional spheres of influence. It’s because the still strong U.S. dollar may be entering a prolonged period of weakening (is Jay Powell still Fed Chair right now? Lemme check). And it’s because there is a national security reason why the U.S. is poking around in places like Greenland and the Ukraine talking about “mineral rights” (the U.S. is not alone in poking around about “mineral rights” btw). It’s because commodities that may not have mattered in aggregate for quite a while are increasingly mattering as we continue through the 2020s.

Does this mean that we run out and go all in on commodities today? Absolutely not. Instead, it means that we shouldn’t summarily dismiss the asset class because it was total return garbage over the past decade. After all, gold had the same “negative returns with high risk” look as commodities at the end of the last millennium following a prolonged bear market that stretched through the 1980s and 1990s (twenty years gone?) at a time when tech stocks were rocking. And in the quarter century that followed from 2000 to 2025, gold has outperformed U.S. stocks by a healthy margin. Could the same be setting up for the broader commodities space today? Only time will tell, but it will take time. Thus, any such portfolio allocations to the category are best made on the margins, which is another way of saying gradually and incrementally if at all.

“The guitar, the drums, the vocals – it all blended into something powerful”

–Jimmy Page, Becoming Led Zeppelin, 2025

Bottom line. All of this highlights a broader important point. Just as a symphony orchestra may have 30 violinists or more performing the melodies, harmonies, and rhythmic support in making beautiful music, and just as Jimmy Page blended 14 guitar tracks in creating an instrumental masterwork for their sixth studio album, an investment portfolio is best served to draw on a variety of different asset classes, categories, and sub-categories that are largely uncorrelated but have the ability to independently generate positive results over time in achieving the powerful harmony of more consistent and predictable risk-managed returns over long-term periods of time. It’s about making beautiful investment music. And this may even include incorporating asset class instruments that may have been gathering dust for years until now.

Disclosure: I/we have no stock, option or similar derivative position in any of the companies mentioned, and no plans to initiate any such positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Investment advice offered through Great Valley Advisor Group (GVA), a Registered Investment Advisor. I am solely an investment advisor representative of Great Valley Advisor Group, and not affiliated with LPL Financial. Any opinions or views expressed by me are not those of LPL Financial. This is not intended to be used as tax or legal advice. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly. Please consult a tax or legal professional for specific information and advice.

LPL Compliance Tracking #: 770889